When I started looking into how insurers evaluate business risk, I noticed that most decisions were built on past records and broad assumptions. A company would be grouped into a category, and pricing or coverage would follow that category. That approach worked to some extent, but it often missed how a business actually operates in real conditions. What has changed now is the way insurers use data, and this is where AI in business insurance risk assessment is making a real difference.

AI in business insurance risk assessment allows insurers to evaluate risk using real-time data, behavioral patterns, and predictive models instead of relying only on historical information. This shift makes underwriting more accurate and helps both insurers and businesses make better decisions before a policy is issued.

How AI in Business Insurance Risk Assessment Changes the Way Risk Is Evaluated

Traditional underwriting focuses on a limited set of inputs such as business type, location, size, and claims history. While these factors are still relevant, they do not always reflect how a business behaves daily. Two companies in the same industry can have completely different risk profiles depending on how they manage operations, safety, and finances.

AI changes this by connecting multiple data sources and analyzing them together. Instead of looking at isolated information, the system identifies relationships between different variables. For example, operational efficiency, employee behavior, and financial stability can all influence risk, and AI models evaluate these factors in combination. This approach makes AI-powered insurance risk assessment more dynamic and aligned with real business conditions.

What Type of Data AI Uses to Assess Business Risk More Accurately

One of the most important differences I’ve seen is the type of data AI systems use. Traditional models depend heavily on internal records and past claims, but AI expands this by including both structured and unstructured data.

This can include financial performance data, operational workflows, supply chain activity, and even external economic signals. When these data points are analyzed together, they provide a clearer picture of how a business is likely to perform in the future. This is why AI-driven risk modeling in commercial insurance is becoming more effective than static evaluation methods.

From my perspective, the value here is not just more data, but better interpretation of that data. AI does not simply collect information; it identifies patterns that indicate potential risk before it becomes visible through traditional metrics.

Predictive Analytics in Business Insurance Risk Assessment

Another major shift comes from predictive analytics. Instead of focusing only on what has already happened, AI models estimate what is likely to happen next based on patterns and trends.

For example, if a business shows signs of financial instability or operational inefficiencies, AI can flag these as potential risk indicators. This allows insurers to adjust coverage, pricing, or conditions before a claim occurs. In practice, predictive risk assessment in insurance helps prevent losses rather than just reacting to them.

I’ve noticed that this forward-looking approach changes the entire underwriting process. It becomes less about reacting to past events and more about anticipating future scenarios.

Faster and More Consistent Underwriting with AI Systems

Speed and consistency are two areas where AI has a clear impact. Manual underwriting takes time because each application requires detailed review. Different underwriters may also interpret the same data in slightly different ways, which can lead to inconsistencies.

AI systems process applications quickly and apply the same evaluation logic across all cases. This reduces delays and improves consistency in decision-making. Businesses benefit from faster quotes, while insurers can handle larger volumes without compromising quality.

This is one reason why automated underwriting systems and AI insurance platforms are becoming standard in modern insurance operations.

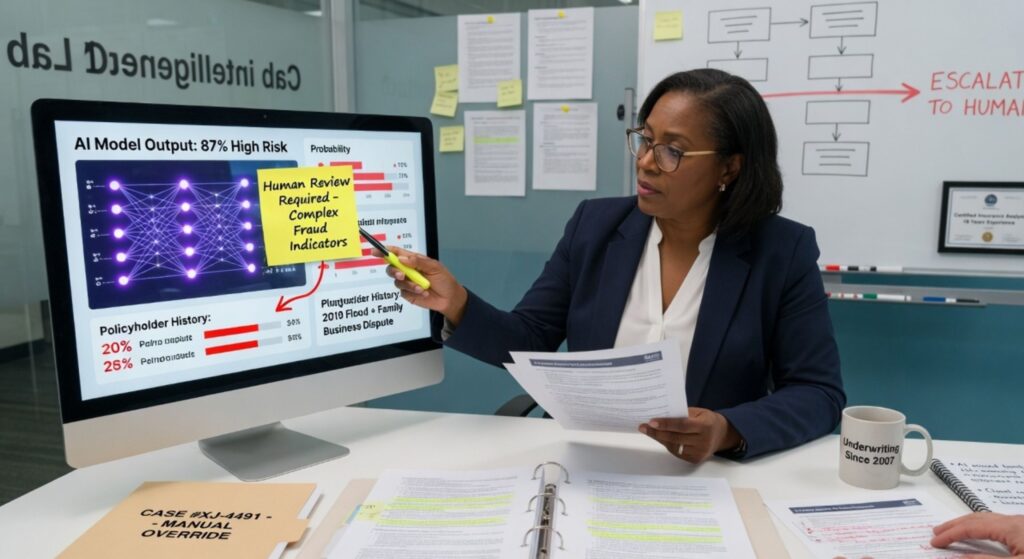

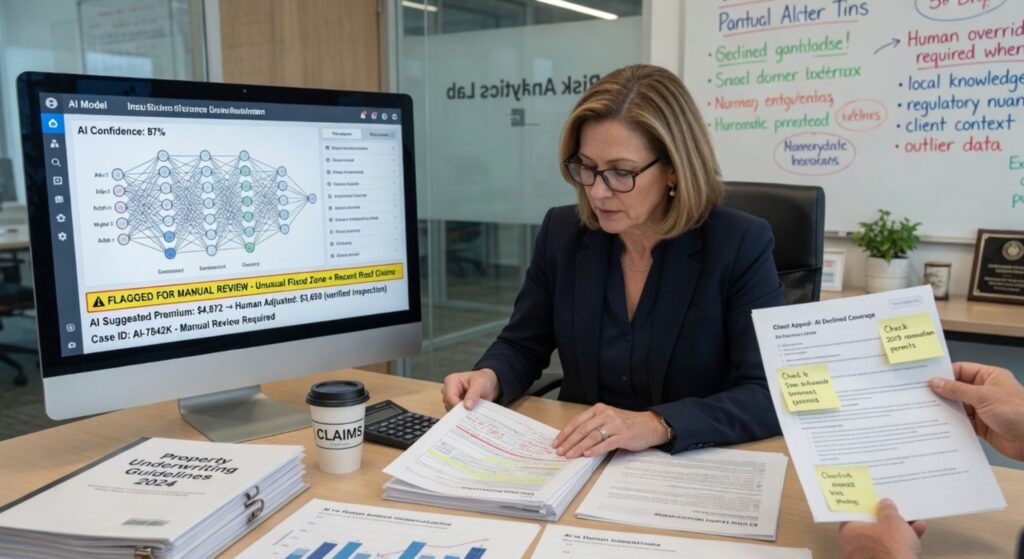

Reducing Bias and Improving Fairness in Risk Assessment

Human judgment is valuable, but it can introduce bias, especially when decisions rely on general assumptions. AI systems focus on data patterns rather than subjective interpretation, which helps create a more consistent evaluation process.

That said, I’ve found that AI works best when it supports human decision-making rather than replacing it. Underwriters still review complex cases and ensure that the final decision makes sense in context. This combination improves both fairness and accuracy.

Continuous Risk Monitoring Beyond Initial Policy Approval

One of the most practical advantages of AI in business insurance risk assessment is that it does not stop at the underwriting stage. AI systems continue to monitor risk even after a policy is issued.

If a business’s operations change, financial conditions shift, or new external risks emerge, the system can detect these changes early. This allows insurers to respond proactively instead of waiting for a claim to reveal the issue.

From what I’ve seen, this continuous monitoring creates a more adaptive insurance model where risk management becomes an ongoing process rather than a one-time evaluation.

How Businesses Benefit from AI-Driven Risk Assessment

The impact of AI is not limited to insurers. Businesses also gain from more accurate and transparent risk evaluation.

They receive pricing that reflects their actual risk profile instead of broad industry averages. They also gain insights into potential weaknesses in their operations, which can help them improve safety and efficiency.

In many cases, this leads to better alignment between coverage and real needs, which reduces both overinsurance and underinsurance.

Where Human Expertise Still Matters in AI-Based Insurance Models

Even with advanced AI systems, human expertise remains essential. Underwriters interpret complex scenarios, validate AI-generated insights, and make final decisions where context matters.

From my experience, the most effective approach is not choosing between AI and human judgment. It is combining both. AI handles data analysis and pattern recognition, while humans ensure that decisions are practical and context-aware.

Why AI in Business Insurance Risk Assessment Is Becoming Essential

The shift toward AI is not just about efficiency. It reflects a deeper change in how risk is understood.

Businesses operate in dynamic environments, and static models cannot fully capture that complexity. AI introduces a level of adaptability that allows insurers to keep up with these changes.

From what I’ve observed, this is why AI in business insurance risk assessment is moving from an optional tool to a core part of the insurance process.

FAQs

AI improves risk assessment by analyzing multiple data sources, identifying patterns, and predicting future risks more accurately than traditional methods.

AI supports underwriters by providing data-driven insights, but human expertise is still needed for complex decisions and final approvals.

AI can lead to more accurate pricing, which may reduce costs for low-risk businesses by aligning premiums with actual risk levels.

Samuel Clarke

Samuel ClarkeSamuel Clarke is an insurance specialist with hands-on experience in policy management, risk assessment, and customer-focused financial protection strategies. He holds a Bachelor’s degree in Business Administration from the University of Florida, He has already built a strong foundation in the insurance industry, having previously worked as an Insurance Manager.