When I started understanding how mortgage loans actually get approved, I realized how slow and rigid the process used to be. Everything depended on paperwork, credit scores, and manual verification. Even small issues could delay approval for weeks. What’s changing now is not just speed, but how lenders evaluate borrowers, and that’s where AI in mortgage loans approval process is making a noticeable impact.

AI in mortgage loans approval process uses machine learning, automated underwriting, and data analysis to evaluate applicants faster and more accurately. It helps lenders verify documents, assess risk, and approve home loans based on a broader financial picture instead of relying only on traditional credit checks.

Why Traditional Mortgage Approval Feels Slow and Limited

If you’ve ever gone through a home loan process, you know how many steps are involved. Lenders ask for income proof, bank statements, employment details, and credit history. After that, everything goes through manual checks.

The problem with this approach is not just the time it takes. It also depends heavily on fixed criteria. If your profile doesn’t fit perfectly into those criteria, approval becomes difficult even if you are financially stable in reality.

From what I’ve seen, this is where many borrowers feel stuck. The system does not always reflect their true financial situation.

How AI Evaluates Mortgage Applications Beyond Credit Scores

One of the biggest changes AI brings is how applications are evaluated.

Instead of focusing only on credit scores, AI systems analyze multiple factors together. These include income patterns, spending behavior, savings consistency, and even transaction history. By looking at how you manage money over time, AI creates a more complete picture of your financial reliability.

For example, someone with an average credit score but stable income and disciplined spending may still qualify under an AI-based system. This is why AI mortgage approval for low credit applicants is becoming more realistic than before.

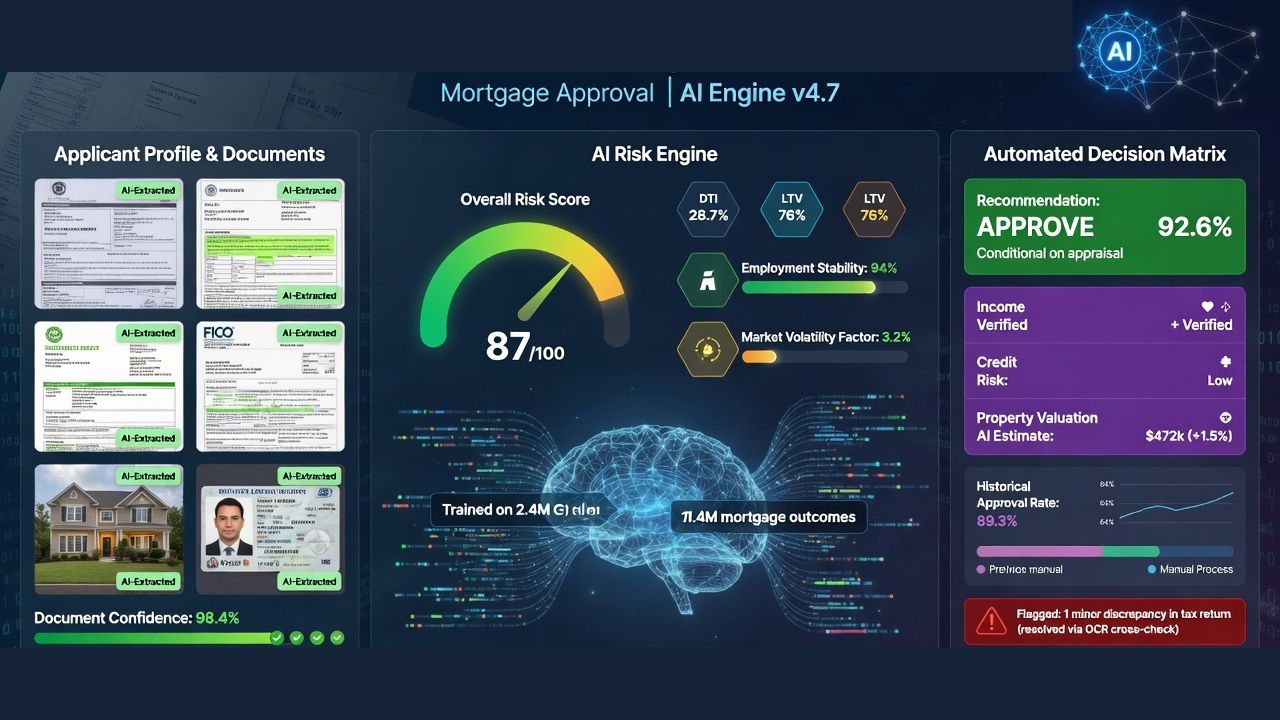

Faster Document Verification in AI Mortgage Loan Processing

Document verification is one of the most time-consuming parts of mortgage approval. AI simplifies this by automatically reviewing documents such as income proofs, tax returns, and bank statements. It can extract key information, verify consistency, and flag discrepancies within minutes.

From my experience observing these systems, this reduces delays significantly. Instead of waiting days for manual checks, lenders can move forward much faster. This is a major reason why digital mortgage approval platforms are gaining popularity.

Automated Underwriting and Risk Assessment with AI

Underwriting is where lenders decide whether to approve a loan and at what terms. AI-powered underwriting systems analyze large datasets to assess risk more precisely. They compare your financial profile with similar cases, identify risk patterns, and calculate the likelihood of repayment.

This does not mean approvals become easier without control. It means decisions become more accurate. Lenders can approve applicants who show strong financial behavior while still managing risk effectively.

This is why AI underwriting in mortgage loans is becoming a core part of modern lending systems.

Real-Time Decision Making in Mortgage Loan Approval

Another change I’ve noticed is how quickly decisions are made. Traditional mortgage approvals can take weeks because every step depends on manual processing. AI systems reduce this time by analyzing data instantly and providing risk insights in real time.

For borrowers, this means faster responses and less uncertainty. You get a clearer idea of your approval chances without waiting for long periods.

This is especially useful in competitive housing markets where timing plays an important role.

How AI Improves Accuracy in Mortgage Loan Pricing

Mortgage pricing depends on how lenders assess risk. With traditional methods, pricing is often based on broad categories. AI improves this by analyzing detailed financial behavior and assigning risk more precisely. This can lead to better interest rates for borrowers who demonstrate stable financial habits.

From what I’ve seen, this creates a more balanced system where pricing reflects actual risk instead of general assumptions.

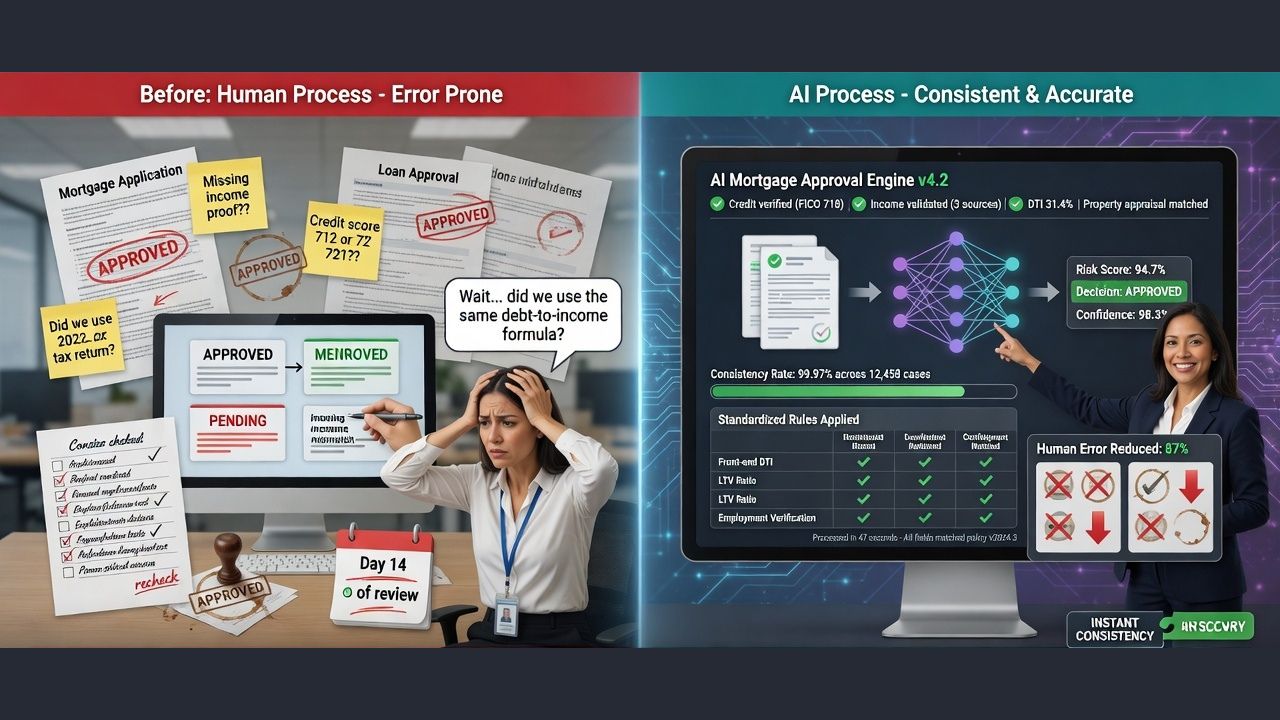

Reducing Human Errors and Improving Consistency

Manual processes always carry the risk of errors. Missing documents, incorrect data entry, or inconsistent evaluation can affect decisions.

AI reduces these issues by standardizing the process. Every application is evaluated using the same logic, which improves consistency and reliability.

At the same time, human oversight still exists for complex cases, ensuring that decisions remain practical and fair.

What This Means for Borrowers in Real Life

The biggest impact of AI in mortgage loans approval process is how it changes the borrower experience.

You get:

- Faster application processing

- More transparent evaluation

- Better chances if your financial behavior is strong

- Reduced dependency on rigid credit score rules

From my perspective, this makes home loan approval feel less unpredictable and more aligned with how you actually manage your finances.

Where You Still Need to Be Careful as an Applicant

Even though AI improves the process, it does not remove the basics.

You still need to:

- Maintain stable income

- Manage your expenses carefully

- Avoid large financial inconsistencies

- Keep your financial records clean

AI helps highlight your strengths, but it also detects risks quickly. So your financial behavior still plays a major role in approval.

Why Mortgage Approval Is Becoming More Data-Driven

What stands out to me is how the entire process is shifting from document-heavy to data-driven. Instead of relying only on what you submit, lenders now analyze how you actually manage money over time. This creates a more realistic evaluation system that benefits both borrowers and lenders.

AI in mortgage loans approval process is not just about faster approvals. It is about making those approvals more accurate and aligned with real financial behavior.

FAQs

Yes, AI speeds up the process by automating data analysis, document verification, and risk assessment, reducing approval time significantly.

No, credit scores are still used, but AI also considers additional financial data, which reduces the reliance on credit scores alone.

AI improves accuracy by analyzing multiple data points and reducing human errors, leading to more reliable decisions.

Kristin Winslow

Kristin WinslowKristin Winslow is a Loan & credit cards specialist with a strong background in consumer finance, focusing on rewards optimization, credit management, and responsible borrowing strategies. She holds a Bachelor’s degree in Finance from the University of Michigan and a certification in Financial Planning from the New York University.