When I first tried to understand why personal loan interest rates vary so much from one borrower to another, the answers always felt incomplete. Most explanations stopped at credit score, income, and debt ratio. But once I looked deeper into how lenders actually price loans today, I realized that those factors are only the starting point.

What really drives modern pricing is how consistently you manage money, and that is exactly what AI in personal loan interest rate calculation is designed to measure.

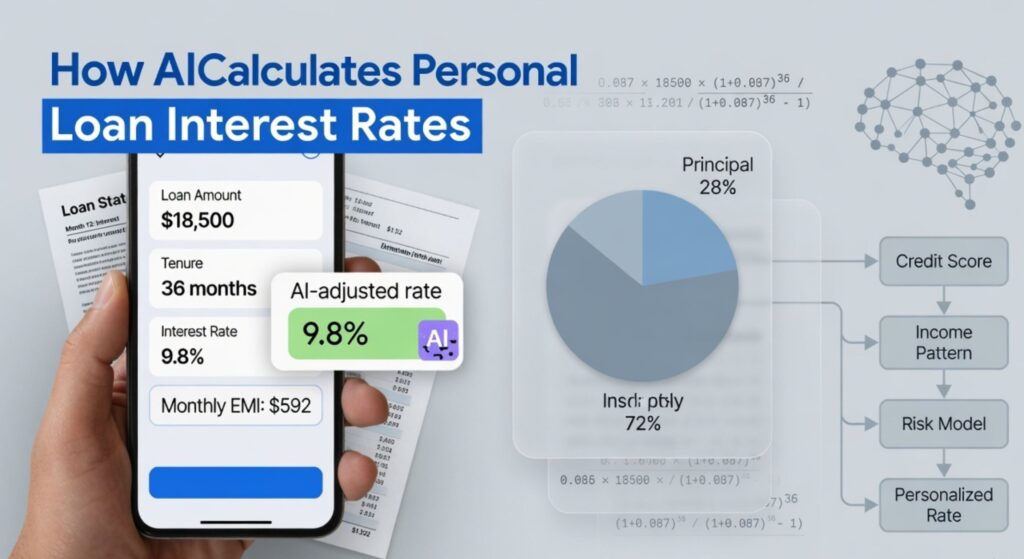

AI in personal loan interest rate calculation uses machine learning models and risk-based pricing systems to evaluate your financial behavior in detail. Instead of placing you into a fixed category, it builds a dynamic risk profile based on how you earn, spend, save, and repay over time.

That profile directly influences the interest rate you receive, which is why two borrowers with similar incomes can still get very different offers.

Why Traditional Loan Interest Calculation Often Felt Inaccurate

Before AI became common in lending, banks relied on structured rules that grouped borrowers into broad categories. Your credit score played the biggest role, followed by income stability and existing debt. While this method was simple to apply, it often missed the reality of how people actually manage their finances.

From what I’ve seen, someone with a decent credit score but inconsistent spending habits could still receive a relatively good rate, while another borrower with disciplined financial behavior but a shorter credit history might be charged more.

The system worked, but it did not always feel fair or accurate. That gap is what pushed lenders toward AI-based loan pricing.

How AI Looks at Your Financial Behavior Instead of Just Your Credit Score

What changed with AI is the depth of analysis. Instead of focusing only on past credit activity, lenders now evaluate patterns in your financial life. AI systems study how regularly your income comes in, how you handle expenses, whether your account balance remains stable, and how often your financial behavior changes.

Read also: AI vs Traditional Loan Approval

When I started analyzing this, one thing became clear. AI is not impressed by a single strong metric. It looks for consistency. A borrower who earns steadily, avoids sudden spending spikes, and maintains a balanced cash flow often appears less risky, even if their credit score is not perfect. That lower risk perception directly leads to more competitive personal loan interest rates.

The Role of Risk-Based Pricing in AI Loan Decisions

At the core of AI loan pricing is risk-based pricing, but it works very differently compared to older systems. Instead of assigning you to a general category, AI compares your financial profile with thousands of similar profiles from past borrowers.

If your behavior matches patterns associated with reliable repayment, the system assigns a lower risk score. That lower risk translates into a lower interest rate. If the data shows irregular income, high volatility in spending, or signs of financial stress, the system adjusts the rate upward to reflect that risk.

From my experience, this approach feels more logical because the pricing is based on behavior, not assumptions.

How Alternative Data Changes Loan Interest Rates

One of the biggest shifts I’ve noticed is the use of alternative data. AI does not stop at traditional credit reports. It can include signals like bill payment consistency, subscription patterns, and overall account activity.

This becomes especially useful for people who do not have a long credit history. Instead of being penalized for limited data, they can still qualify for reasonable rates if their financial behavior shows stability.

This is why you now see more platforms offering personal loans with AI-based underwriting even for borrowers who previously struggled to get approved.

Why AI Can Offer Lower Interest Rates to the Right Borrowers

AI does not automatically reduce interest rates for everyone, but it creates opportunities for borrowers who manage their finances well. When lenders understand risk more accurately, they do not need to overprice loans to protect themselves.

Read also: AI in Mortgage Loans

From what I’ve observed, this leads to more competitive rates for disciplined borrowers because the uncertainty is lower. At the same time, it ensures that higher-risk profiles are priced appropriately, which keeps the system balanced.

What You Can Do to Improve Your AI-Based Loan Interest Rate

Even though AI handles the calculation, your behavior still drives the outcome. Maintaining stable income, avoiding sudden financial disruptions, and keeping your spending consistent all contribute to a stronger profile.

What I’ve personally found is that small habits matter more than big changes. Regular savings, controlled expenses, and timely payments create patterns that AI systems recognize quickly. Over time, these patterns can lead to better loan offers and lower interest rates.

Where AI Loan Pricing Still Has Limits

AI improves accuracy, but it is not perfect. It depends heavily on the data it receives, and not every financial situation fits neatly into a model. Some borrowers may still find that their unique circumstances are not fully captured by automated systems.

There is also the question of data usage, since these models rely on detailed financial information. While this improves decision-making, it also requires careful handling of privacy and transparency.

A More Realistic Way to Understand Personal Loan Interest Rates Today

What I’ve come to understand is that personal loan interest rates are no longer based on a simple formula. They reflect how you manage your finances over time, not just how you performed in the past.

AI in personal loan interest rate calculation is making lending more precise and more behavior-driven. For borrowers, this means your daily financial habits matter more than ever. For lenders, it means better risk control and more accurate pricing.

FAQs

AI analyzes income patterns, spending behavior, and financial stability to assign a risk score, which determines the interest rate.

Yes, if your financial behavior shows consistency and low risk, AI-based systems can offer more competitive rates.

No, credit scores are still used, but AI adds more data layers to improve accuracy.

Kristin Winslow

Kristin WinslowKristin Winslow is a Loan & credit cards specialist with a strong background in consumer finance, focusing on rewards optimization, credit management, and responsible borrowing strategies. She holds a Bachelor’s degree in Finance from the University of Michigan and a certification in Financial Planning from the New York University.