When I first compared home loan offers from different lenders, I assumed the interest rate mostly depended on credit score and income. That explanation sounded simple, but it never fully explained why rates still varied so much between similar borrowers.

Once I started looking deeper into how lenders actually price mortgages today, it became clear that AI in home loan interest rate calculation is changing the process in a much more detailed and practical way.

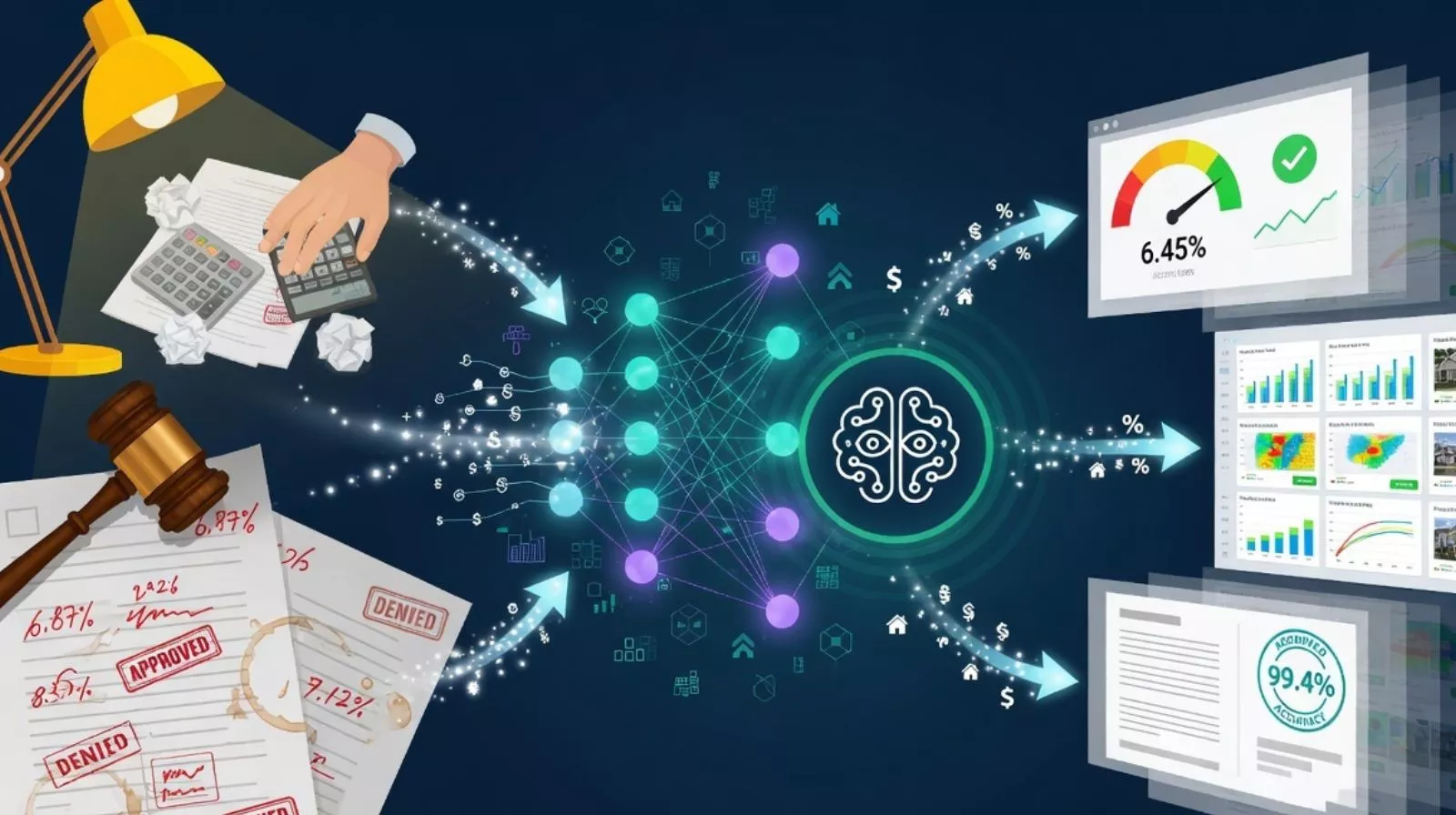

AI in home loan interest rate calculation uses machine learning models, real-time data analysis, and risk-based pricing to evaluate borrowers beyond traditional metrics. Instead of assigning a fixed rate based on a few inputs, it builds a detailed financial profile and adjusts the interest rate according to how reliably you are expected to repay the loan over time.

Why Home Loan Interest Rates Were Traditionally Limited

In earlier systems, lenders relied on a structured formula. Credit score, income stability, debt-to-income ratio, and loan amount formed the base of every decision. While this method created consistency, it often missed the full picture of a borrower’s financial behavior.

From what I’ve seen, two applicants with similar credit scores could receive different rates, but the reasoning behind that difference was not always clear. The system depended on broad categories, which made pricing less precise than it should have been. This limitation is exactly what AI-based mortgage pricing is solving.

How AI Evaluates Borrowers for Mortgage Interest Rates

AI does not stop at surface-level data. It looks deeper into how you manage your finances over time. Instead of focusing only on your credit report, AI systems analyze income consistency, spending patterns, savings behavior, and overall financial stability.

Read also: AI vs Traditional loans approval process

These patterns help determine how likely you are to handle long-term repayment, which is critical in a mortgage that may last decades.

What I’ve noticed is that consistency matters more than isolated data points. A borrower who shows steady financial habits often appears less risky, even if their credit score is not perfect. This directly influences the interest rate offered.

Risk-Based Mortgage Pricing Using AI Models

The foundation of AI-driven mortgage pricing is risk-based analysis, but it works in a more refined way compared to traditional systems.

AI compares your financial profile with thousands of past borrowers who had similar characteristics. If your behavior aligns with profiles that showed strong repayment performance, the system assigns a lower risk score. That lower risk leads to a more favorable home loan interest rate.

If the data shows irregular income, high financial volatility, or signs of instability, the system adjusts the rate upward to reflect that increased risk.

From my perspective, this approach feels more aligned with real financial behavior rather than general assumptions.

How Property Data and Market Trends Influence AI Calculations

Home loans are different from personal loans because the property itself plays a role in risk assessment.

AI models include property-related data such as location trends, property value stability, and local market conditions. If a property is in a stable or growing market, the perceived risk decreases. If the market shows volatility, the risk increases.

What stands out to me is how AI connects borrower data with market data. This creates a more complete evaluation where both personal financial behavior and external conditions influence the final interest rate.

Real-Time Data and Dynamic Interest Rate Adjustments

One major advantage of AI is how quickly it processes information. Traditional mortgage pricing could take days or weeks because it depended on manual checks. AI systems evaluate data instantly and adjust rates based on current financial and market conditions.

From what I’ve observed, this makes the process more responsive. Rates reflect real-time insights instead of relying on outdated or static data.

How AI Improves Accuracy in Mortgage Rate Decisions

Accuracy improves when more relevant data is included in the decision process. AI reduces the chances of overpricing or underpricing a loan because it evaluates multiple variables together.

Lenders can price loans more confidently, and borrowers receive rates that better reflect their actual risk profile.

What I’ve found interesting is that this reduces the gap between how lenders perceive risk and how risk actually exists in real life.

What You Can Do to Get a Better AI-Based Home Loan Interest Rate

Even though AI handles the calculations, your financial behavior still shapes the outcome. Maintaining stable income, managing expenses carefully, and avoiding sudden financial changes all contribute to a stronger profile. Over time, these patterns improve how AI systems evaluate your risk.

From my experience, consistency in financial habits has a greater impact than trying to optimize one single factor like credit score.

Where AI Mortgage Pricing Still Has Limitations

AI improves the system, but it does not eliminate all challenges. It depends on data quality, and not every financial situation fits neatly into a model. Some borrowers may still find that their unique circumstances are not fully captured.

There are also considerations around data usage, since these systems rely on detailed financial information. While this improves accuracy, it requires responsible handling of data.

A More Practical Way to Understand Mortgage Interest Rates Today

What I’ve come to understand is that home loan interest rates are no longer based on a simple checklist. They reflect a deeper analysis of how you manage money and how stable your environment is over time.

AI in home loan interest rate calculation is making mortgage pricing more precise, more dynamic, and more aligned with real-world behavior. For borrowers, this means your financial habits matter more than ever. For lenders, it creates a system that manages risk more effectively.

FAQs

AI analyzes financial behavior, income stability, property data, and market trends to assign a risk score that determines the interest rate.

Yes, consistent financial behavior and low-risk profiles can lead to more competitive rates in AI-based systems.

No, AI enhances underwriting by adding more data and improving accuracy, while human oversight still exists.

Kristin Winslow

Kristin WinslowKristin Winslow is a Loan & credit cards specialist with a strong background in consumer finance, focusing on rewards optimization, credit management, and responsible borrowing strategies. She holds a Bachelor’s degree in Finance from the University of Michigan and a certification in Financial Planning from the New York University.