High-risk drivers pay less overall with liability insurance unless they finance a vehicle or own something worth more than $4,000–$5,000. Liability meets every state’s minimum requirements and SR-22 filings while covering damage you cause to others.

Full coverage adds collision and comprehensive protection for your own car, yet it routinely doubles or triples your premium on an already expensive high-risk policy. You choose based on your vehicle’s actual cash value, your loan status, and how much cash you can spare if your car gets totaled tomorrow.

High-risk drivers those with recent DUIs, at-fault accidents, or multiple tickets already battle premiums 2–3 times higher than clean-record drivers. Picking the wrong coverage either drains your budget or leaves you on the hook for thousands in repairs.

This breakdown gives you the exact differences, current 2026 numbers, and the decision framework that actually saves you money.

What Liability Insurance Covers for High-Risk Drivers

Liability pays for injuries and property damage you cause to other people and their vehicles. Every state except New Hampshire requires it. High-risk drivers usually need an SR-22 filing a simple certificate your insurer sends to the DMV to prove they carry at least the state minimum limits.

The policy never touches your own car. Crash into a guardrail? You pay the repairs yourself. Hit another driver? Liability steps in up to your policy limits.

Most states set minimums around 25/50/25 (bodily injury per person/per accident and property damage), though high-risk drivers often carry higher limits to satisfy courts or lenders.

How Full Coverage Differs—and What It Adds

Full coverage is not a single product. Insurers combine your required liability with two optional pieces: collision (repairs your car after you hit something) and comprehensive (theft, fire, hail, floods, falling trees, or vandalism). You still get the liability protection; you simply add the physical-damage layers on top.

Lenders demand full coverage until you pay off the loan. Even without a loan, you keep it when your car’s value exceeds the annual premium cost of those add-ons.

Drop collision and comprehensive once your car’s worth drops below roughly 10 percent of what full coverage would cost you yearly that rule keeps more money in your pocket.

Why High-Risk Drivers Face Higher Premiums Either Way

Your driving record signals higher odds of a claim. Insurers respond with rate hikes. According to Forbes Advisor’s 2026 analysis, drivers who need SR-22 coverage after a DUI pay an average of $3,295 per year.

Bankrate’s nationwide data shows standard full coverage at $2,697 annually and minimum liability at $820, yet high-risk profiles routinely push liability-only into the $1,800–$5,600 range with $3,000 as a realistic average for many after a serious violation.

Those numbers explain why you feel sticker shock. The same factors that made you high-risk—accidents, speeding tickets, or lapses in prior coverage apply to both policy types. Liability stays cheaper because it omits your vehicle’s repair costs.

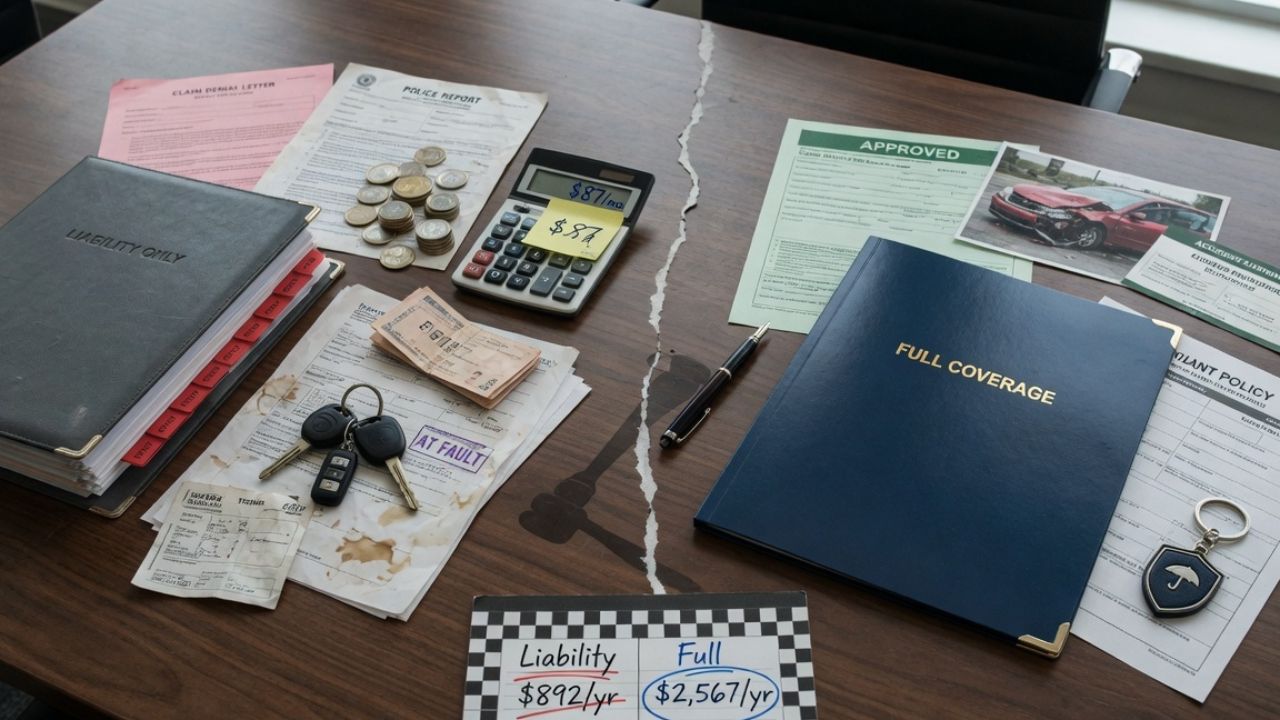

Cost Breakdown: Liability vs Full Coverage for High-Risk Drivers in 2026

Expect liability-only SR-22 policies to land between $1,800 and $5,600 yearly depending on your state, violation, and insurer. Full coverage adds collision and comprehensive and typically increases that bill by 80–150 percent more.

A driver with a recent DUI might pay $3,000 for liability-only versus $5,000–$7,000 for full coverage in the same ZIP code.

Real example from current data: a 40-year-old with one DUI in a mid-size city often sees liability quotes around $250–$350 monthly. Full coverage jumps to $400–$600 monthly. Shop three carriers because the spread between the cheapest and most expensive quote for identical high-risk coverage can exceed $2,000 a year.

When Liability Insurance Beats Full Coverage for You

Choose liability when your car is paid off and worth less than $4,000–$5,000. You can replace or repair it out of pocket if something happens.

You also pick liability when every extra dollar counts and you drive an older, lower-value vehicle. The savings let you build an emergency fund that actually covers a total loss.

High-risk drivers with older cars who switch to liability-only routinely cut their annual bill by $1,500–$3,000. That money compounds faster than the risk of self-insuring a $3,000 vehicle.

When Full Coverage Makes Financial Sense Despite the Price

Keep or add full coverage if you still owe money on the car lenders require it. You also keep it when your vehicle’s value sits above $8,000–$10,000 and you lack the cash to replace it outright.

High-risk drivers who commute long distances or park on the street in high-theft or hail-prone areas gain real protection from the added layers.

Read also: AI in Car Insurance Quotes Pricing

Collision and comprehensive become worth the premium once your car’s replacement cost exceeds the extra annual outlay. Run the math: if full coverage costs you $2,000 more per year and your car is worth $15,000, you break even after roughly 7–8 years of claims-free driving. Below that threshold, you self-insure.

Smart Ways High-Risk Drivers Cut Insurance Costs

Raise your deductible on collision and comprehensive to $1,000 or $2,000. Maintain continuous coverage lapses trigger bigger hikes. Shop every six months because high-risk rates shift fast as your record ages.

Ask about discounts for completing a defensive-driving course or installing a telematics device that tracks safe habits. Bundle with homeowners or renters insurance for an automatic 10–25 percent shave. Non-owner SR-22 policies can cost $600–$1,800 yearly if you rarely drive your own car.

Pick the Coverage That Matches Your Wallet and Your Wheels

Liability gives high-risk drivers the lowest legal premium and satisfies every SR-22 filing. Full coverage adds meaningful protection only when your car’s value justifies the extra cost or your lender forces your hand.

Run the numbers on your specific vehicle today, compare three quotes with the exact same liability limits, then add collision and comprehensive only if the math works.

Start by pulling your current policy and your car’s current market value. Get fresh quotes this week. The right choice will cut hundreds or even thousands from your annual bill while keeping you fully legal and driving.

FAQs

No. SR-22 only proves you carry your state’s minimum liability limits. You can file it with liability-only unless your lender demands more.

High-risk profiles pay 2–3 times more on average. A DUI alone can add 79 percent or more to your premium, according to industry data.

Yes. Once the loan clears and your car’s value drops low enough that you could replace it cash, you can switch to liability-only and pocket the difference.

Your policy covers the other driver’s damages up to your limits. You pay for your own car repairs or replacement out of pocket.

Samuel Clarke

Samuel ClarkeSamuel Clarke is an insurance specialist with hands-on experience in policy management, risk assessment, and customer-focused financial protection strategies. He holds a Bachelor’s degree in Business Administration from the University of Florida, He has already built a strong foundation in the insurance industry, having previously worked as an Insurance Manager.