When I started looking into student loans, most options felt the same. Lenders focused heavily on credit scores, co-signers, and fixed approval criteria. If you didn’t fit that structure, getting approved became difficult. What I’ve noticed recently is a shift in how some lenders approach this problem. Instead of relying only on traditional metrics, they are using AI to understand a student’s real potential, not just their past financial history.

AI in student loan risk assessment is changing how lenders evaluate applicants by analyzing education, future income potential, and financial behavior instead of depending only on credit scores. This makes student loans more accessible, especially for those who are just starting their financial journey.

Why Student Loan Approval Needed a Different Approach

Student lending has always been unique compared to other types of loans. Most applicants do not have a long credit history, and many are still studying or just entering the workforce. Traditional risk models struggle in this situation because they depend on past financial data that simply does not exist for many students.

From what I’ve seen, this creates a gap where capable students get rejected or need a co-signer, even when they have strong future earning potential. This is exactly the problem AI-based student loan companies are trying to solve by looking at forward-looking indicators instead of only past records.

How AI Evaluates Students Beyond Credit Scores

The biggest difference with AI-based student loan risk assessment is what gets analyzed. Instead of focusing only on credit history, these systems look at factors like:

- Field of study and degree type

- School reputation and completion likelihood

- Expected future income based on career path

- Financial behavior patterns where available

What stands out to me is that this approach feels more realistic. A student studying in a high-demand field with strong earning potential is evaluated differently from someone in a less predictable path, even if both have limited credit history.

This is why AI-based student loan approval without cosigner is becoming more common.

Top Student Loan Companies Using AI for Risk Assessment

Upstart

From what I’ve observed, Upstart is one of the earliest platforms to apply AI in lending decisions. While it is not limited to student loans, it uses education, job history, and income potential as part of its risk model.

This makes it useful for borrowers who may not have strong credit but have a stable career path ahead. The system looks at more than just numbers on a credit report, which improves approval chances.

SoFi

SoFi focuses heavily on student loan refinancing, but what makes it stand out is how it evaluates applicants. It considers career trajectory, income growth potential, and financial stability.

From my experience reviewing such platforms, this approach works well for graduates who are early in their careers but show strong earning potential over time.

CommonBond

CommonBond uses data-driven models to assess borrower profiles and offer competitive rates. While the AI aspect is not always visible to users, it plays a role in evaluating risk and pricing.

What I’ve noticed here is a focus on balancing risk with accessibility, especially for students from reputable programs.

Earnest

Earnest takes a slightly different approach by analyzing financial habits in detail. It looks at savings behavior, spending patterns, and income consistency.

This creates a more personalized evaluation compared to traditional lenders. From what I’ve seen, this helps borrowers get rates that reflect their actual financial discipline.

Prodigy Finance

For international students, Prodigy Finance uses AI and data models to assess future earning potential rather than requiring a local credit history.

This is a significant shift because international students often struggle with traditional lending requirements. AI allows the platform to evaluate risk based on education and career prospects instead.

Climb Credit

Climb Credit focuses on career-focused education programs and uses outcome-based data to assess risk. It evaluates whether a program leads to employability and income growth.

From what I’ve observed, this aligns lending decisions with real-world outcomes rather than just academic credentials.

What Makes AI-Based Student Loan Companies Different

The key difference is not just technology. It is the mindset behind how risk is evaluated. Traditional lenders look at what you have done financially in the past. AI-based lenders try to understand what you are likely to achieve in the future. That shift changes the entire approval process.

From my perspective, this approach is more suitable for students because it aligns with how their financial journey actually begins.

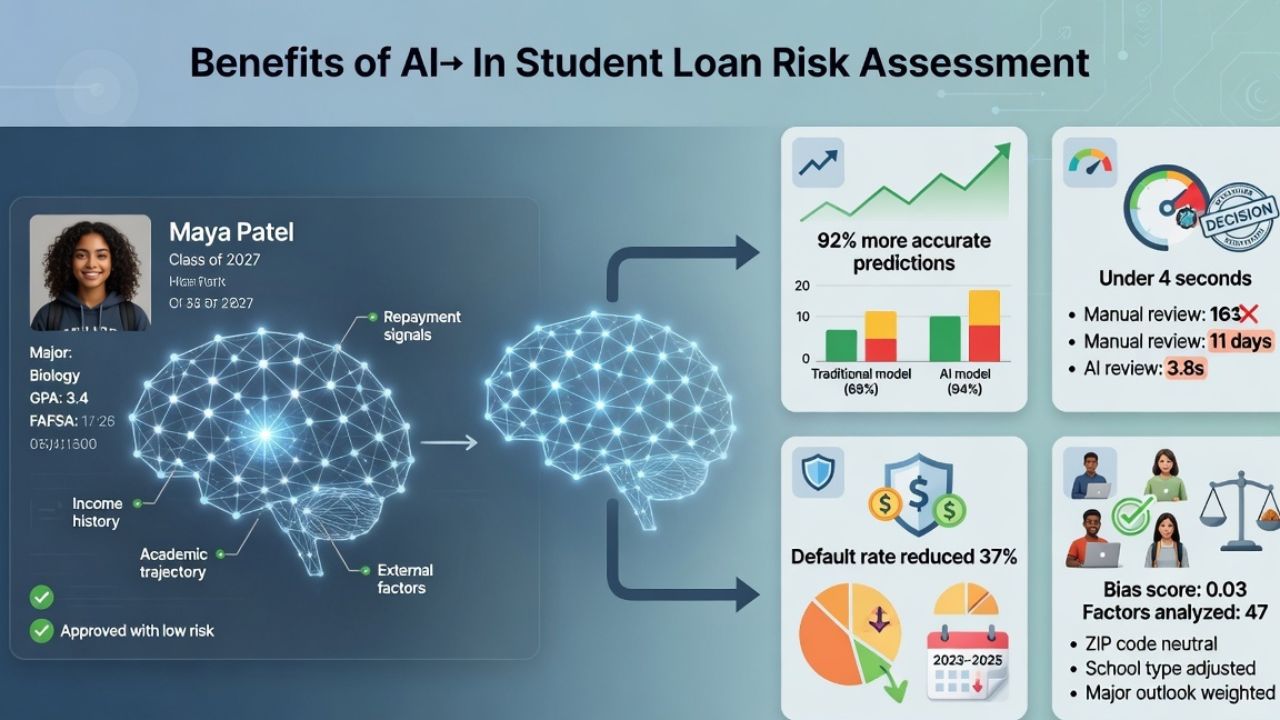

Benefits of AI in Student Loan Risk Assessment

AI-based student loan platforms offer several practical advantages. They improve approval chances for applicants without strong credit history, reduce dependency on co-signers, and provide more personalized interest rates.

At the same time, they make the process faster and more transparent because decisions are based on structured data analysis rather than manual review alone.

Where You Still Need to Be Careful

Even though AI improves access, it does not remove responsibility. You still need to consider repayment ability, future income stability, and loan terms carefully. AI helps lenders make better decisions, but it does not guarantee that a loan will be easy to repay.

From what I’ve seen, the best approach is to use these platforms as an opportunity, not a shortcut.

A More Practical Way to Understand Student Loan Risk

The biggest change I’ve noticed is how risk is being redefined. Instead of judging students based on limited financial history, AI allows lenders to evaluate potential. This makes student loans more aligned with real-world career paths and earning opportunities.

AI in student loan risk assessment is not just improving approvals. It is creating a system that better understands how students grow financially over time.

FAQs

Companies like Upstart, SoFi, Earnest, and Prodigy Finance use AI or data-driven models to evaluate borrower profiles beyond traditional credit scores.

Yes, some AI-based lenders evaluate future income potential, which reduces the need for a co-signer.

They can be more flexible and accessible, but you still need to evaluate terms and repayment ability carefully.

Kristin Winslow

Kristin WinslowKristin Winslow is a Loan & credit cards specialist with a strong background in consumer finance, focusing on rewards optimization, credit management, and responsible borrowing strategies. She holds a Bachelor’s degree in Finance from the University of Michigan and a certification in Financial Planning from the New York University.